By 2025, renewables would be the dominant source of electricity supply at 40 per cent, followed by coal and gas

During a recent webinar organised by the Malaysian Oil & Gas Engineering Council (MOGEC), Dr Wei-nee Chen, VP of New Energy Ventures of Hibiscus Petroleum Bhd, was invited to speak on Energy Transition: Global and Local Medium Outlook of Renewable Energy.

Wei-nee was previously Chief Strategic Officer of the Sustainable Energy Development Authority (SEDA) of Malaysia. After 15 years in the renewable energy sector serving the Ministry of Energy in Putrajaya, she joined the oil and gas to pursue her passion in the energy transition in that sector.

Running out of Time

At the start of her presentation, Dr Wei-nee expressed the energy transition’s urgency to share the global carbon budget. According to a report from the IPCC (2018), the global carbon budget for a 50 per cent probability of 1.5oC temperature increase is less than 500 Gt of CO2, and there is a window of 11.5 years remaining.

If this is brought forward to 2021, that window translates to less than 10 years. The Covid-19 pandemic caused a drop the GHG emissions by a record low of seven per cent in 2020 alone. This translated to an average temperature increase of 2.1oC by the end of this century.

While emissions due to Land Use, Land Use Change and Forestry (LULUCF) remained more or less constant for the past century, the rapid increase of emissions is mainly due to the burning of fossil fuel (Exhibit 1).

In 2019, coal contributed nearly 40 per cent of the global emissions, whereas oil & gas contributed about 55 per cent.

Resilience of Renewables during Pandemic

While Covid-19 has caused the oil price to collapse and most sectors to a near economic standstill, renewables were among the few industries that have witnessed tremendous growth.

Specifically, there was a strong demand for wind and solar, thanks to the green economic recoveries that most countries had in place coupled with increasing stakeholders’ pressure for corporates to embrace ESG investments.

The rapid decline in the cost of solar and wind energy also accelerated their growth. In October 2020, the IEA declared that solar was the cheapest form of energy. It is breaking one record after another, boosted by improving competitiveness.

The IEA also acknowledged that renewables were set to grow aggressively. By 2025, renewables would be the dominant electricity supply source at 40 per cent, followed by coal and gas.

The Covid-19 pandemic has shed light on what a climate crisis could look like. Not surprising, today, the drive to accelerate energy transition comes from our race to achieve nett zero carbon emissions.

Nett Zero: Will we get there?

As of 2020, we had nearly 130 countries declaring their commitment to nett zero carbon emissions by 2050, including leading corporates. Despite the pledges, will we get there?

The bad news is that the IEA (2020) showed that the existing and emerging technologies today would not be sufficient to reach global nett zero goals. There is a need for more innovations to close our residual gap to get the nett zero goal.

Stakeholders need to be on board and be committed to operationalise the nett zero goal. This includes the government, the industry, financial institutions, and civil society.

What does this mean to the oil & gas sector?

The good news is that oil majors have demonstrated their environmental stewardship by announcing their nett zero targets for their Scope 1 and 2.

Some notable oil majors such as Shell, BP, Equinor, Repsol, and Occidental Petroleum have expanded their nett zero commitment to Scope 3.

In Malaysia, we are very proud that Petronas has led by example by being the first oil company in Asia to set a nett zero target.

“Hibiscus Petroleum Bhd, with operating assets in Malaysia and UK, recently declared to become a nett zero emissions producer and adopt energy transition as one of our core business drivers,” said Wei-nee.

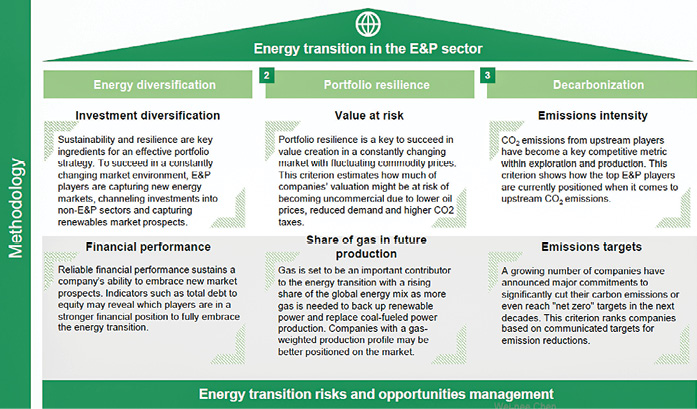

Energy Transition for Oil & Gas Sector: According to a study by Rystad Energy, the E&P sector focuses on three pillars of energy transition (Exhibit 2).

These pillars are energy diversification, portfolio resilience and decarbonisation. E&Ps typically invest in renewables (e.g. solar, offshore wind), low carbon technologies (EVs, batteries), and digitalisation/automation in energy diversification.

Investments that include renewable energy production could help reduce their Scope 3 emissions and reduce their carbon intensity of aggregate energy produced.

Some E&Ps focus to improve the resilience of their portfolio of assets by managing the financial risks of their investments with regards to exposure to fluctuating oil prices, possible drop in demand (due to increasing electrification of mobility) and imposition of the carbon tax in certain jurisdictions.

While the long-term oil demand is likely to decline, gas will increase in demand due to its role as bridging fuel in managing the intermittency of solar and wind in the electricity grid. Unlike oil which cannot be decarbonised, gas can be decarbonised.

The final pillar of energy transition applies to all E&P companies, which is decarbonisation. Decarbonisation is an essential aspect of the energy transition, and for the upstream, this will reduce emissions from combustion, flaring, and venting.

What’s in it for the OFS industry?

While the Covid-19 pandemic has caused severe job cuts for the oil & gas sector, Wei-nee shared findings by Rystad Energy which revealed that oilfield service suppliers (OFS) could diversify some O&G capabilities and replace up to 40 per cent of 2019’s revenue by servicing the renewable markets.

Specifically, contractors providing EPCI services will find it easier to apply their competencies towards the green shift. This includes expanding their services to supply the end-to-end development and operations of renewable power generation.

However, some services may be challenging to deploy in the context of energy transition operations, e.g. seismic, G&G, OCTG, drilling services and tools, as they are deemed as less relevant in the energy transition space.

Most traditional oilfield service suppliers are looking to expand into low carbon segments, meaning technologies or services aiming to reduce or prevent emissions from oil and gas E&P activities. This can be done by offering more efficient operations and digital solutions.

Another emerging market within the energy transition is clean energy infrastructure, where suppliers can provide services to support blue or green hydrogen infrastructure, CCS, or energy storage in general.

This is a market where engineering houses, fabricators, and equipment manufacturers will find growth opportunities and synergies. Wei-nee cited a few examples in which OFS have diversified, leveraging on their core skills.

For instance, Sapura Energy in 2019 announced an award for offshore wind turbine substructures in Taiwan as part of an offshore wind farm with a total capacity of 640MW.

In another example, she highlighted a global oilfield service provider, Schlumberger, which collaborated with LafargeHolcim to explore CCS development in two of LafargeHolcim’s cement plants in Europe and North America, using Schlumberger’s CCS technologies.

Challenges are plenty, but we only have one planet

Wei-nee concluded by sharing some challenges faced in the energy transition. These included balancing the energy trilemma for policymakers to achieve energy security, energy affordability and environmental sustainability.

In closing her remarks, Wei-nee said: “We only have a window of fewer than 10 years for the global carbon budget, and we must remember we only have one planet for our children. They do not have plan(et) B”. — @green

{kind=link}